Originally posted on K-Ratio

Trucking is a commodity and like any commodity, its price, though volatile and unpredictable, is still subject to the principles of supply and demand. In 2020, these principles, and their derivative concepts, were stressed and stretched to their very limits but always held true. One would be hard pressed to find another calendar year containing as many economic cycles as the prior. Unfortunately, or perhaps fortunately depending on which business one is in, 2021 will likely pick up and continue right where 2020 left off. Despite the extreme seasonality typically found inside freight, markets do not stop or

revert to normal conditions simply because we turn the page to a new set of days. Rather, all elements of seasonality and past historical trends should only exacerbate the extremes of supply, demand, and their intersection: price.

Volatility is here to stay. The freight industry was already in the midst of an evolutionary change when Covid-19 hit. The industry’s response to it has been a much-need real-time exercise in digitization and modernization. Working from home became the norm with automation of some tasks and outsourcing of others. Headcounts have been reduced while factoring and nearshoring have grown. Freight has resisted change for years, incrementally allowing minimal advancement at its own pace. Last March, an unforeseen external event took every Fred Flintstone of freight out of their foot-driven vehicle, not quite into George Jetson’s flying car, but at least into the 21st Century. The juxtaposition of a volatile rate landscape set inside a rapidly changing industry environment will serve both as the force of reckoning for companies unwilling or unable to adapt and the bounty of riches for those positioned to innovate.

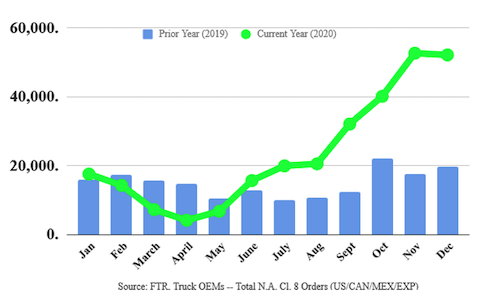

Today we find ourselves in a demand rather than supply market. The story isn’t about too many trucks like 2019 or the distribution and rebalancing of them and their limits like in 2018. The only aspect of supply by way of truck capacity affecting today’s marketplace is that we just do not have enough of them. Adding to that, just when it feels like we might be getting close to an equilibrium, the heavy fragmentation of the market rears its head and primary markets short on trucks shift the entire country into a new gear higher for rates.

The mythical driver shortage saga remains a hot industry topic despite the fact that we ended 2020 with 10.7 million unemployed Americans. Shuttered driving schools due to pandemic lockdowns is acknowledged, but given the boom/bust/boom pattern in rates seen, this situation is more likely one of driver recruitment and retention than an all out shortage. Crete, Schneider, Covenant, A&R, KLLM, Roehl, C.R. England, Stevens, and Heartland are just some of the companies that have publicly announced driver pay increases for 2021. While the purpose here to attract new and retain current drivers, the message sent to the rest of the industry is undoubtedly that contract rates are going higher. Judging by some of the pay increases, a double-digit increase has moved from possible to probable.

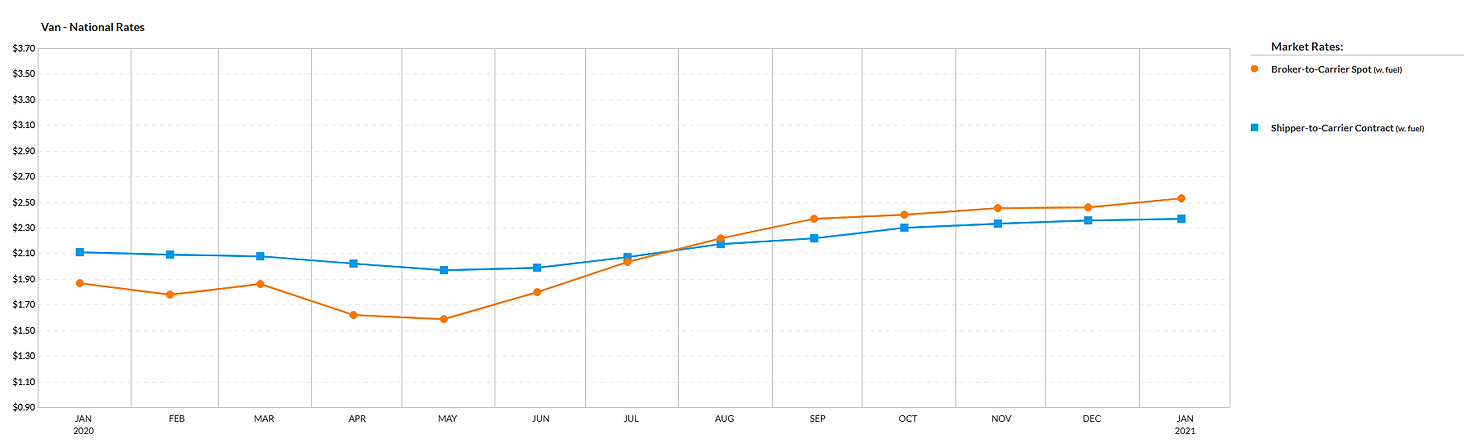

Shifting to the other side of the price equilibrium brings us to the biggest question in the industry today. How long will demand stay strong? That’s a tough question in normal times but in a post (current?)-Covid world, it’s anybody’s guess. Last year we saw the predictable then unpredictable response. Volumes jumped during the panic buying spree only to plummet into the abyss shortly after. The resurrection out of the hole is what caught everyone off guard. Was that response from the US Consumer a one-off reaction or part of a dramatic alteration in behavior? That is the real question.

The most significant influence on rates for 2021 might just come from a uniquely freight occurrence. The annual bid cycle, briefly mentioned earlier, will definitely bring higher rates, the question is just how much higher. A marginal move higher in dedicated rates might bring satisfaction to Shippers, but that pleasant feeling will not last. Only a sharp increase, beyond single digits, will be enough to pull loads back from the spot market and into routing guides. Anything less will allow this current situation to persist longer than most desire.

Categorically external but a result of internal dynamics, the flow of imported goods will be the most important factor at play here. Should the current trend of excessive Port of LA/Long Beach imports persist, the LA/Ontario markets will continue to act as the primary driver of the national supply chain. High volumes will demand high rates to move them and all capacity west of the Mississippi will act accordingly. Time, so far, has not been a friend to Shippers, removing the option of maritime transport through the Panama Canal and reducing the desire for rail, even if rail capacity was available. Should this scenario change, it would dramatically alter the current level of truck capacity demand and the repositioning of fleets to more easterly locations would take significant time while creating havoc across RPMs by location. Overall, such a move would weaken rates nationally as a more balanced network with more balanced volumes fits better into national freight portfolios than everyone jamming into Southern California.

US economic conditions continue to be overshadowed by surging Covid infection numbers with vaccine hopes dominating financial market opinions. Equity bulls call for a repeat of the Roaring Twenties once we hit critical mass in vaccinations. Equity bears draw parallels to the Great Depression and its lingering effects. Neither one matters much as it pertains to freight. Investment capital has and will continue to flood the industry as long as the Federal Reserve continues to print money. This excess liquidity is deflationary to freight rates as it allows recent, well-funded entrants to the marketplace the ability to absorb losses longer than traditional businesses. This could have some effect during the bid cycle if better capitalized firms see 2021 as an opportunity to win market share and/or eliminate some competitors. With the worst of the pandemic as it pertains to freight seemingly behind us, greater investment in trucks and trailers seems likely, especially if volumes remain firm. This would provide a divergent H1/H2 scenario where more capacity enters the space in the back half of the year, subsequently driving down spot rates at a time when volumes will be in question.

A new presidential administration will be sworn in on January 20. No significant transportation or commerce specific policies are expected, but attention should be paid to the US-China relationship and a possible warming of the cold trade war. Developments in this area would be friendly to our import arrangement and would further embolden LA as the primary driver of the domestic supply chain. On the topic of China, Lunar New Year once again will create a mini pull-forward at a time when domestic truck capacity cannot handle it.

A Tale of Two Halves by John Q. Broker. Not quite a literary masterpiece but the story written and told by every 3PL in 2021. It’s hard to envision today’s current situation abruptly coming to an end. Inventory rebuilds are underway and both truck deliverables and annual RFP awards are several weeks, if not months away. Even when the first trucks show up and the newest lane awards enact at higher rates, it will take a certain critical mass to stem the flow of rising rates. Thinking practically about timing, the industry will be deep into produce season with the seasonal summertime bump just on the horizon. Hard to imagine rates buckling prior to those major events.

Looking ahead to the back half of 2021 is a different story altogether. July traditionally marks the start of a volume pullback and when coupled with the potential for some added capacity to get delivered while new award rates take effect, the combination of just two, if not three, of these events would certainly remove the inflationary pressure on prices and likely exert some downward pressure, as well. Of course, all of this is predicated on the return to normal.

Should. Hopefully.

[1] FTR Associates, 01/2021 [2] CBS News, 04/2020 [3] FreightWaves’ SONAR platform, 01/2021

“If we learned anything from 2020, it’s that supply chains need to evolve, ” said Jaimie Kowalski Sleek Technologies VP Marketing. “Manufacturers are shifting to smart tech and digitization to update old processes to cut waste and become more agile.” #SleekPOV

Join our newsletter. click here